Dairy updates

Strong demand offsets headwinds, but milk supplies continue to build.

Strong export demand continues to support dairy markets, but growing milk supplies are weighing on prices. USDA's May Milk Production report showed U.S. milk production increased 2.3% year over year, driven by both herd expansion and higher milk output per cow. The national dairy herd grew by approximately 10,000 head in May, while upward revisions to April data added another 10,000 cows, extending a trend of steady growth fueled in part by strong beef-on-dairy economics and historically high calf values.

Export markets remain the strongest source of demand for the dairy sector. April marked the seventh consecutive month of year-over-year export growth, with U.S. dairy exports increasing 15% on a milk-solids-equivalent basis. Through the first four months of 2026, exports were up 12% from the same period last year, representing the strongest start to a year on record. Cheese continues to lead export growth, with April volumes reaching a record high and increasing 30% year over year, while butterfat exports also posted impressive gains thanks to competitive U.S. pricing and strong shipments into Middle Eastern markets.

Milk prices are expected to remain under pressure despite strong export performance. Expanding milk production, ample product inventories, and softer domestic demand have created headwinds for prices. After an impressive rally earlier this year, nonfat dry milk and cheese prices have begun to soften as supply growth matches demand. While whey prices have remained comparatively stable due to continued consumer demand for protein products, Class III and Class IV milk futures are generally expected to remain rangebound through the remainder of 2026. Future price direction will likely depend on export demand, currency values, and broader economic conditions.

Dairy fundamentals across AgWest's territory remain generally positive, supported by healthy milk checks, robust processor demand and strong beef revenues. However, producers are increasingly balancing those positives against higher feed costs, drought-related water concerns, and expectations for tighter margins in the months ahead. As a result, operational efficiency, risk management, and financial discipline remain top priorities for dairy operations in the West.

Strong beef-on-dairy economics continue to provide an important financial cushion for many producers. Arizona dairies reported day-old calf values near $1,800 per head, helping offset milk price volatility and support profitability. Favorable milk checks during the second quarter and widespread use of Dairy Revenue Protection (DRP) programs have further strengthened margins. At the same time, extreme heat has reduced alfalfa quality and lowered winter wheat yields in parts of Arizona, while similar feed-related challenges have emerged elsewhere in the West.

Water availability is a continued risk across much of AgWest's dairy territory. Although many Arizona dairies rely primarily on groundwater and face less immediate exposure to Colorado River shortages, water uncertainty continues to shape producer decisions throughout the West. California producers are closely monitoring litigation surrounding groundwater extraction fees in the Tulare Lake Subbasin. Idaho has seen a variety of water allocations lowered following a statewide declaration of drought declared in April.

Highly Pathogenic Avian Influenza (HPAI) cases have increased alongside spring bird migrations, with Idaho accounting for most recent dairy detections in June. While current impacts on milk production remain limited and HPAI does not pose food safety concerns for dairy products, producers are closely monitoring developments. Any broader resurgence of HPAI could temporarily reduce milk output and add volatility to markets.

The outlook for the remainder of 2026 remains cautiously optimistic. Strong export demand, healthy processor demand, and favorable beef-on-dairy economics continue to support margins, but expanding milk supplies, elevated input costs, and ongoing water concerns are creating a less favorable market environment.

Profitability

June 10, 2026Dairy: Slightly profitable - Neutral 12-month outlook

Improving milk prices and relatively low feed costs, combined with added revenue from elevated beef values, support modest profitability.

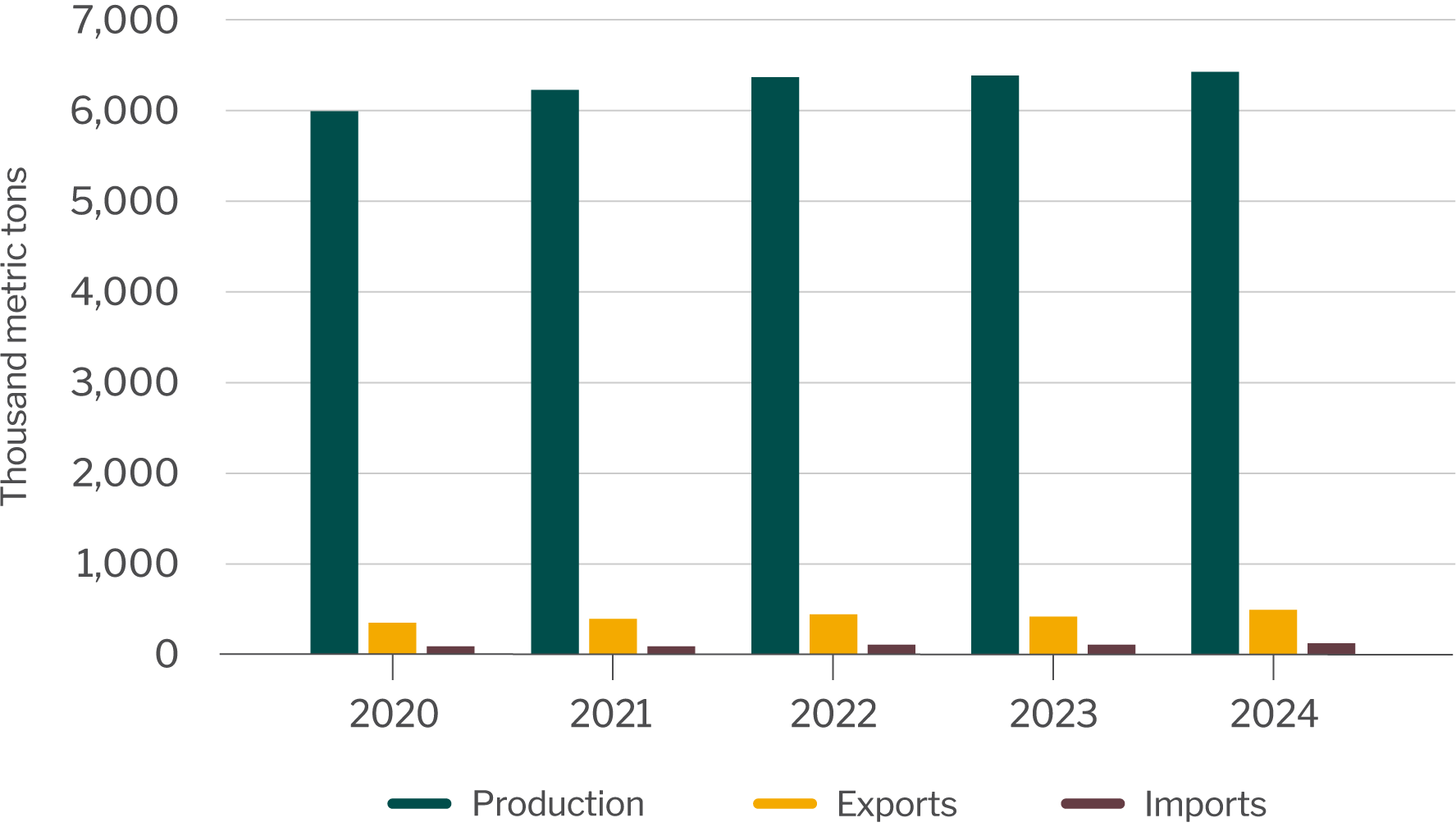

The U.S. ranks as the second-largest exporter of dairy products, following the European Union. Over 15% of U.S. dairy production is exported. Mexico and Canada are the top destinations, accounting for more than 40% of total exports. Key U.S. dairy exports include nonfat dried milk, skim milk powder, cheese, whey, lactose, butter and other products. For cheese, major export markets include Mexico, South Korea, Japan and Canada.

The U.S. also imports a significant amount of cheese, primarily from the European Union. Many of these imported cheeses carry geographic indicators, signifying they originate from specific regions and are uniquely tied to those areas. This designation prevents others from replicating such cheeses outside their original region, ensuring their distinctiveness.

Cheese production, exports and imports

Source: USDA National Agriculture Statistics Service. U.S. Census Bureau.

Tariff tracker - Tariff rates applied to U.S. trade partners are consistenly updated to reflect policy changes. The World Trade Organization (WTO) tracks duties and tariffs on dairy products. For your convenience, the following links will take you to tariff data on cheddar cheese (a leading U.S. export for the dairy industry) for top markets including South Korea and Japan. Dairy products are currently exempt from tariffs for Mexico and Canada under the United States-Mexico-Canada Agreement (USMCA), but please refer to the U.S. Trade Representative website for up-to-date information. WTO also tracks rates for dairy imports to the U.S. Please consult with a trade lawyer or professional for detailed and up-to-date insights on tariff rates and their application to dairy products.

For guidance on interpreting duty and tariff rates, please refer to our Tariff Guide.

Dairy updates

Strong demand offsets headwinds, but milk supplies continue to build.

Strong export demand continues to support dairy markets, but growing milk supplies are weighing on prices. USDA's May Milk Production report showed U.S. milk production increased 2.3% year over year, driven by both herd expansion and higher milk output per cow. The national dairy herd grew by approximately 10,000 head in May, while upward revisions to April data added another 10,000 cows, extending a trend of steady growth fueled in part by strong beef-on-dairy economics and historically high calf values.

Export markets remain the strongest source of demand for the dairy sector. April marked the seventh consecutive month of year-over-year export growth, with U.S. dairy exports increasing 15% on a milk-solids-equivalent basis. Through the first four months of 2026, exports were up 12% from the same period last year, representing the strongest start to a year on record. Cheese continues to lead export growth, with April volumes reaching a record high and increasing 30% year over year, while butterfat exports also posted impressive gains thanks to competitive U.S. pricing and strong shipments into Middle Eastern markets.

Milk prices are expected to remain under pressure despite strong export performance. Expanding milk production, ample product inventories, and softer domestic demand have created headwinds for prices. After an impressive rally earlier this year, nonfat dry milk and cheese prices have begun to soften as supply growth matches demand. While whey prices have remained comparatively stable due to continued consumer demand for protein products, Class III and Class IV milk futures are generally expected to remain rangebound through the remainder of 2026. Future price direction will likely depend on export demand, currency values, and broader economic conditions.

Dairy fundamentals across AgWest's territory remain generally positive, supported by healthy milk checks, robust processor demand and strong beef revenues. However, producers are increasingly balancing those positives against higher feed costs, drought-related water concerns, and expectations for tighter margins in the months ahead. As a result, operational efficiency, risk management, and financial discipline remain top priorities for dairy operations in the West.

Strong beef-on-dairy economics continue to provide an important financial cushion for many producers. Arizona dairies reported day-old calf values near $1,800 per head, helping offset milk price volatility and support profitability. Favorable milk checks during the second quarter and widespread use of Dairy Revenue Protection (DRP) programs have further strengthened margins. At the same time, extreme heat has reduced alfalfa quality and lowered winter wheat yields in parts of Arizona, while similar feed-related challenges have emerged elsewhere in the West.

Water availability is a continued risk across much of AgWest's dairy territory. Although many Arizona dairies rely primarily on groundwater and face less immediate exposure to Colorado River shortages, water uncertainty continues to shape producer decisions throughout the West. California producers are closely monitoring litigation surrounding groundwater extraction fees in the Tulare Lake Subbasin. Idaho has seen a variety of water allocations lowered following a statewide declaration of drought declared in April.

Highly Pathogenic Avian Influenza (HPAI) cases have increased alongside spring bird migrations, with Idaho accounting for most recent dairy detections in June. While current impacts on milk production remain limited and HPAI does not pose food safety concerns for dairy products, producers are closely monitoring developments. Any broader resurgence of HPAI could temporarily reduce milk output and add volatility to markets.

The outlook for the remainder of 2026 remains cautiously optimistic. Strong export demand, healthy processor demand, and favorable beef-on-dairy economics continue to support margins, but expanding milk supplies, elevated input costs, and ongoing water concerns are creating a less favorable market environment.

Profitability

June 10, 2026Dairy: Slightly profitable - Neutral 12-month outlook

Improving milk prices and relatively low feed costs, combined with added revenue from elevated beef values, support modest profitability.

The U.S. ranks as the second-largest exporter of dairy products, following the European Union. Over 15% of U.S. dairy production is exported. Mexico and Canada are the top destinations, accounting for more than 40% of total exports. Key U.S. dairy exports include nonfat dried milk, skim milk powder, cheese, whey, lactose, butter and other products. For cheese, major export markets include Mexico, South Korea, Japan and Canada.

The U.S. also imports a significant amount of cheese, primarily from the European Union. Many of these imported cheeses carry geographic indicators, signifying they originate from specific regions and are uniquely tied to those areas. This designation prevents others from replicating such cheeses outside their original region, ensuring their distinctiveness.

Cheese production, exports and imports

Source: USDA National Agriculture Statistics Service. U.S. Census Bureau.

Tariff tracker - Tariff rates applied to U.S. trade partners are consistenly updated to reflect policy changes. The World Trade Organization (WTO) tracks duties and tariffs on dairy products. For your convenience, the following links will take you to tariff data on cheddar cheese (a leading U.S. export for the dairy industry) for top markets including South Korea and Japan. Dairy products are currently exempt from tariffs for Mexico and Canada under the United States-Mexico-Canada Agreement (USMCA), but please refer to the U.S. Trade Representative website for up-to-date information. WTO also tracks rates for dairy imports to the U.S. Please consult with a trade lawyer or professional for detailed and up-to-date insights on tariff rates and their application to dairy products.

For guidance on interpreting duty and tariff rates, please refer to our Tariff Guide.