Forest product updates

Lumber prices gain slightly as industry enters peak construction season.

Lumber prices increased moderately in June due to tightening supplies and flat demand. Flat to declining production levels in the U.S. and reduced imports from Canada have lowered softwood lumber supply. The housing market remains flat overall, with single family home sales and starts down in both April and May. Multi-family home starts fell by 42% in May, one of the largest drops on record. Regionally, conditions are mixed as homebuyers increasingly prioritize affordability. The West is experiencing broad declines in home values while gains are observed in the Midwest and South. Congress passed the 21st Century Road to Housing Act (the Act), though it remains unclear if President Trump will sign it. The Act is a comprehensive bill intended to increase housing supply and affordability by reducing regulatory barriers, encouraging local housing development, expanding affordable housing programs, supporting manufactured housing, and limiting the role of large institutional investors in the single-family housing market.

Log markets across Oregon and Washington remained generally stable to firm through June, supported by steady mill demand and adequate inventories. Demand is strongest for larger-diameter Douglas-fir, specialty logs, cedar, poles, and veneer-quality timber, while smaller sawlogs continue to face limited outlets and weaker pricing. Mills are actively buying but doing so conservatively due to housing market concerns.

Profitability

June 10, 2026Forest product mills: Breakeven profitability - Neutral 12-month outlook

Timberlands: Slightly profitable - Neutral 12-month outlook

Low homeowner affordability continues to weigh on the housing market, resulting in relatively weak wood product demand and prices.

Log demand is limited as wood product mills face a weak housing market.

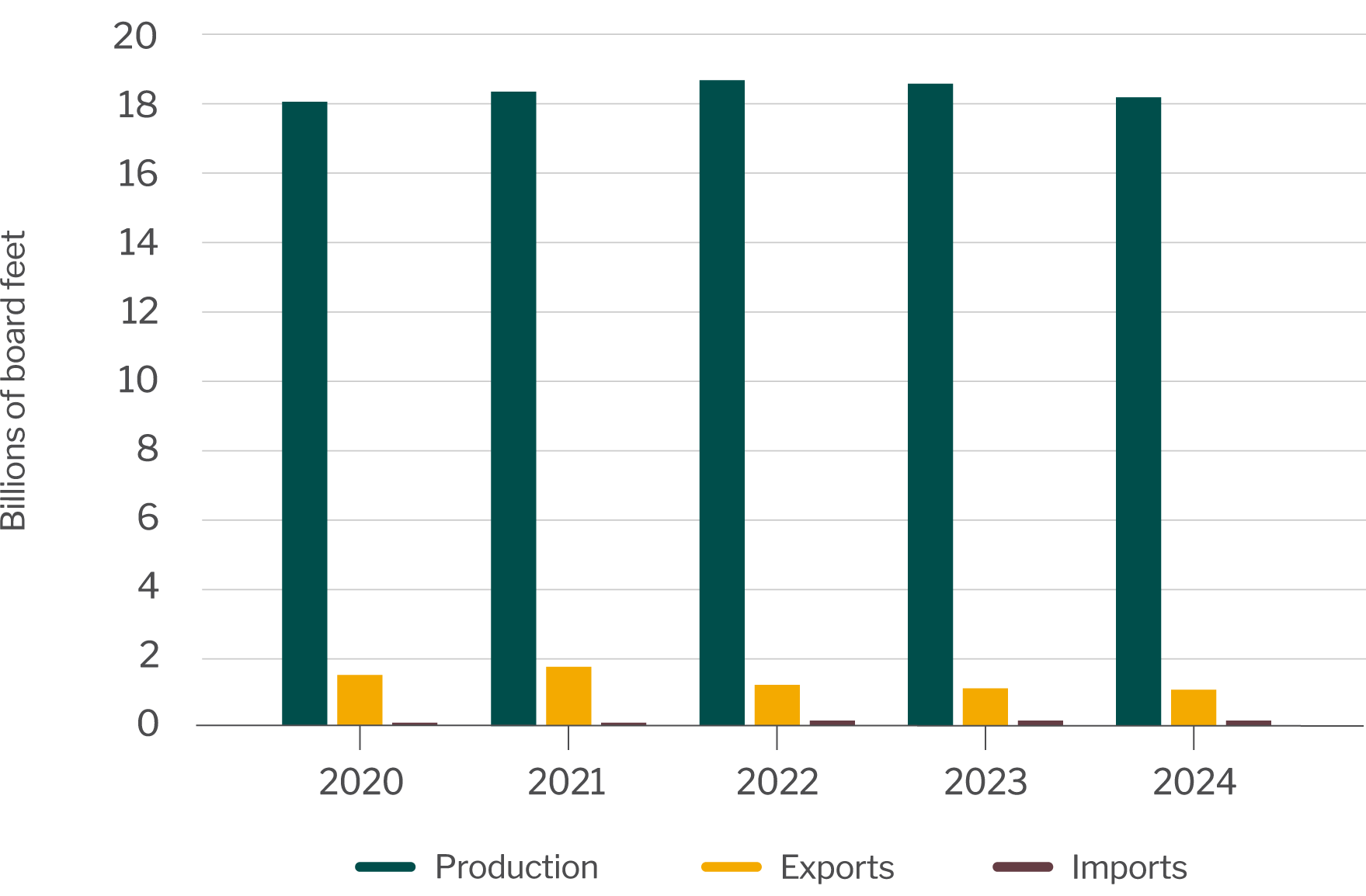

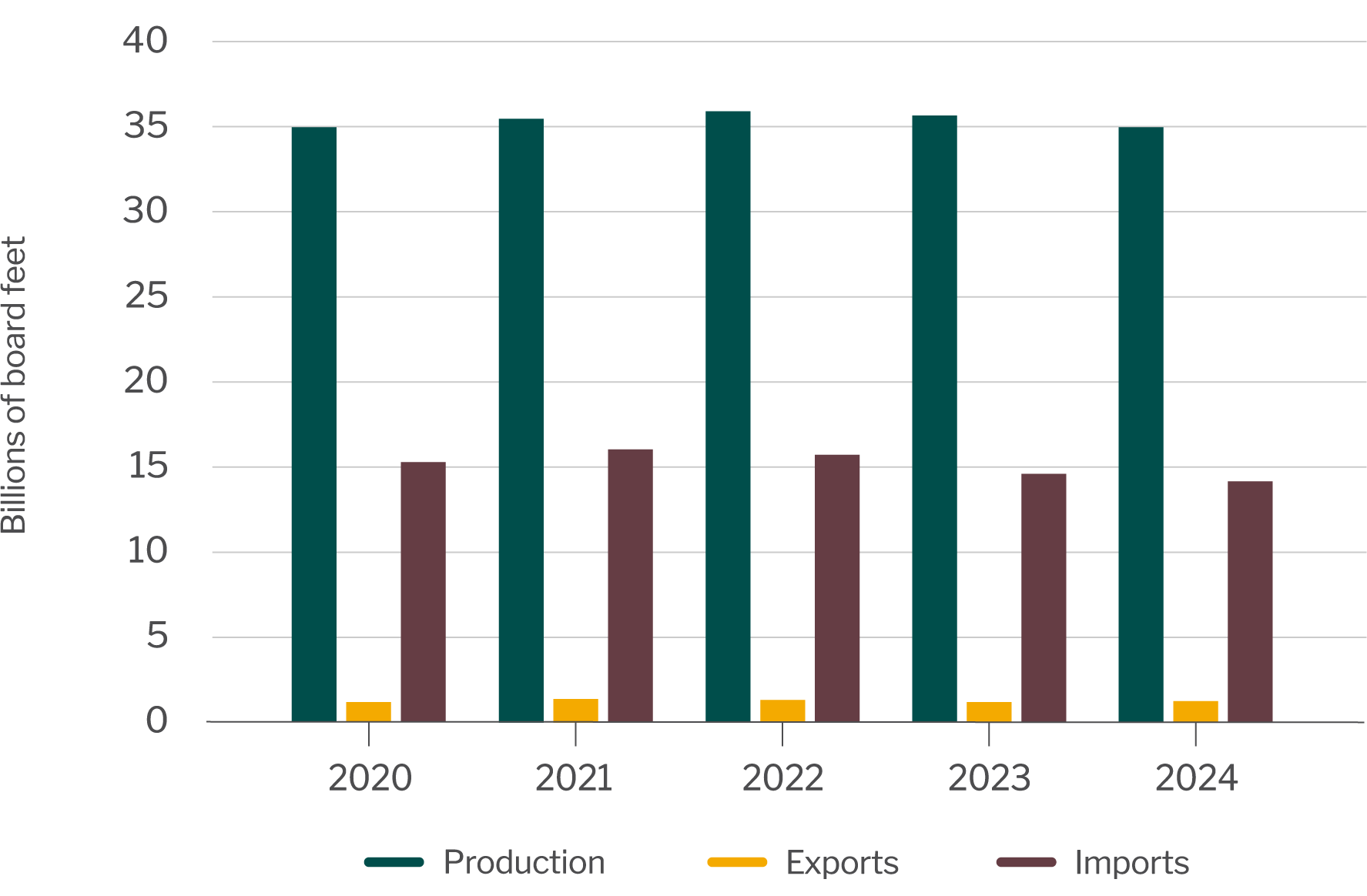

The U.S. housing market is the primary driver of forest products demand. Log and lumber exports play a relatively minor role, making up about 6% and 3% of total domestic production, respectively. On the West Coast, log producers have historically benefited from strong Japanese demand for high-quality grades. Following the Great Recession, demand from China increased significantly to support housing construction. These trends are reversing due to aging demographics and weakening economies. The Softwood Lumber Agreement sets the terms for Canadian lumber exports to the U.S., which make up about a quarter of total domestic supply.

Log production, exports and imports

Forisk. U.S. Census Bureau. Production levels were calculated using region specific recovery rates. Trade data was converted using .22 thousand board feet per cubic meter.

Lumber production, exports and imports

Forisk. U.S. Census Bureau. Trade data was converted using .452 thousand board feet per cubic meter.

Tariff tracker - Tariff rates applied to U.S. trade partners are consistenly updated to reflect policy changes. The World Trade Organization (WTO) tracks duties and tariffs on forest products. For your convenience, the following links will take you to tariff data for top markets, including Japan and Vietnam. Logs are currently exempt from tariffs for Canada under the United States-Mexico-Canada Agreement (USMCA), but please refer to the U.S. Trade Representative website for up-to-date information. The U.S. applies countervailing duties on Canadian lumber imports based on an annual review process (detailed information can be found at the Federal Register). Please consult with a trade lawyer or professional for detailed and up-to-date insights on tariff rates and their application to forest products.

For guidance on interpreting duty and tariff rates, please refer to our Tariff Guide.

Forest product updates

Lumber prices gain slightly as industry enters peak construction season.

Lumber prices increased moderately in June due to tightening supplies and flat demand. Flat to declining production levels in the U.S. and reduced imports from Canada have lowered softwood lumber supply. The housing market remains flat overall, with single family home sales and starts down in both April and May. Multi-family home starts fell by 42% in May, one of the largest drops on record. Regionally, conditions are mixed as homebuyers increasingly prioritize affordability. The West is experiencing broad declines in home values while gains are observed in the Midwest and South. Congress passed the 21st Century Road to Housing Act (the Act), though it remains unclear if President Trump will sign it. The Act is a comprehensive bill intended to increase housing supply and affordability by reducing regulatory barriers, encouraging local housing development, expanding affordable housing programs, supporting manufactured housing, and limiting the role of large institutional investors in the single-family housing market.

Log markets across Oregon and Washington remained generally stable to firm through June, supported by steady mill demand and adequate inventories. Demand is strongest for larger-diameter Douglas-fir, specialty logs, cedar, poles, and veneer-quality timber, while smaller sawlogs continue to face limited outlets and weaker pricing. Mills are actively buying but doing so conservatively due to housing market concerns.

Profitability

June 10, 2026Forest product mills: Breakeven profitability - Neutral 12-month outlook

Timberlands: Slightly profitable - Neutral 12-month outlook

Low homeowner affordability continues to weigh on the housing market, resulting in relatively weak wood product demand and prices.

Log demand is limited as wood product mills face a weak housing market.

The U.S. housing market is the primary driver of forest products demand. Log and lumber exports play a relatively minor role, making up about 6% and 3% of total domestic production, respectively. On the West Coast, log producers have historically benefited from strong Japanese demand for high-quality grades. Following the Great Recession, demand from China increased significantly to support housing construction. These trends are reversing due to aging demographics and weakening economies. The Softwood Lumber Agreement sets the terms for Canadian lumber exports to the U.S., which make up about a quarter of total domestic supply.

Log production, exports and imports

Forisk. U.S. Census Bureau. Production levels were calculated using region specific recovery rates. Trade data was converted using .22 thousand board feet per cubic meter.

Lumber production, exports and imports

Forisk. U.S. Census Bureau. Trade data was converted using .452 thousand board feet per cubic meter.

Tariff tracker - Tariff rates applied to U.S. trade partners are consistenly updated to reflect policy changes. The World Trade Organization (WTO) tracks duties and tariffs on forest products. For your convenience, the following links will take you to tariff data for top markets, including Japan and Vietnam. Logs are currently exempt from tariffs for Canada under the United States-Mexico-Canada Agreement (USMCA), but please refer to the U.S. Trade Representative website for up-to-date information. The U.S. applies countervailing duties on Canadian lumber imports based on an annual review process (detailed information can be found at the Federal Register). Please consult with a trade lawyer or professional for detailed and up-to-date insights on tariff rates and their application to forest products.

For guidance on interpreting duty and tariff rates, please refer to our Tariff Guide.

IN THIS SECTION

![]()

Forest Products Industry Perspective

View the latest AgWest Forest Products Industry Perspective

Learn more