Hay updates

Western producers see price improvements, but water remains the wild card.

Hay markets across the West are entering the second half of 2026 in a stronger position than a year ago, supported by higher prices, limited carryover stocks and steady demand. However, ongoing drought conditions, irrigation uncertainty and water allocation challenges remain the biggest risks to production and profitability through the remainder of the growing season.

Across AgWest's footprint, acreage trends remain relatively stable, suggesting supply-side adjustments are unlikely to significantly alter market dynamics through the remainder of the season.

Conditions by state:

Arizona

Hay quality has declined due to early-season heat, though demand for lower-quality forage remains supportive. Prices are generally around $200 per ton, with expectations for modest improvement if weather cooperates. Water availability remains a significant concern, particularly given anticipated Colorado River shortages and the potential for reduced allocations under future drought contingency plans.

California

Market conditions remain favorable, with producers reporting stronger prices than expected. In the Southern San Joaquin Valley, third cutting has been completed with no major yield or weather concerns due to irrigated production systems. Producers reported hay prices approximately $30 per ton above last year, with recent third-cutting alfalfa selling near $225 per ton. Demand appears supported by both dairy and retail channels. In Imperial Valley, growers are seeing prices around $200-$205 per ton, and continue utilizing deficit irrigation programs amid growing concerns about Colorado River water supplies and the potential for future allocation reductions.

Idaho

The market remains firm, with prices generally steady to $5 per ton higher than a month ago and above year-ago values. Demand is uneven, as some dairies remain on the sidelines while others actively contract supplies. Cattle ranchers have been among the most aggressive buyers due to ongoing drought concerns. Water availability remains the state's primary challenge. Several irrigation districts have warned of possible late-season water curtailments, prompting some growers to prioritize corn irrigation over hay production. Southern and eastern Idaho are increasingly concerned that reduced water allocations will limit second and third cuttings, while some farmers reliant on mountain runoff have already lost irrigation water. Well-irrigated operations are generally in a better position. Concerns are growing in eastern Idaho that many operations may only achieve a single cutting this year. Organic hay markets remain especially firm.

Montana

Dryland hay conditions in southern Montana range from poor to very poor due to spring freezes, drought, high temperatures, and wind. In contrast, northern Montana has recently received substantial rainfall, improving yield expectations to near-average or potentially above-average levels. Irrigated hay producers experienced poor first-cutting yields due to freeze damage but are optimistic about stronger second and third cuttings. Hay supplies remain tight, with much of the available crop already committed. New-crop high-quality alfalfa has sold between $225-$230 per ton, utility hay around $200 per ton, and wheat hay near $170 per ton. Strong cattle-sector demand and ongoing drought concerns continue to support prices.

Oregon

Hay growers are increasingly focused on water availability as drought conditions worsen. Several irrigation districts may impose water restrictions later this summer, creating concerns about maintaining production through subsequent cuttings. Despite these risks, first cutting has progressed well, with producers actively baling and preparing for second cutting. Demand for old-crop hay remains slow, while interest in new-crop supplies has improved. Hay quality and yields generally look favorable, aided by cooler temperatures and timely moisture. Baker Valley producers reported 2026 alfalfa sales near $250 per ton.

Washington

Market conditions continue to improve compared to 2025. Limited carryover inventories have supported higher prices, with alfalfa values generally running $20-$30 per ton above last year's levels. Higher-quality alfalfa is trading around $215-$220 per ton, feeder hay near $175 per ton, and premium Timothy horse hay between $235-$240 per ton. While profitability has improved, rain events during first cutting created some quality variability, though yields are generally average.

Profitability

June 10, 2026Hay (alfalfa): Slightly profitable - Bullish 12-month outlook

Hay (timothy): Slightly profitable - Neutral 12-month outlook

Tightening Western supplies and an expected reduction in hay production are helping rebalance the market, while increasing drought concerns are driving stronger domestic demand and improving alfalfa prices.

Sustained export demand, limited high-quality supply and steady forage demand are supporting timothy hay profitability despite higher production and logistics costs.

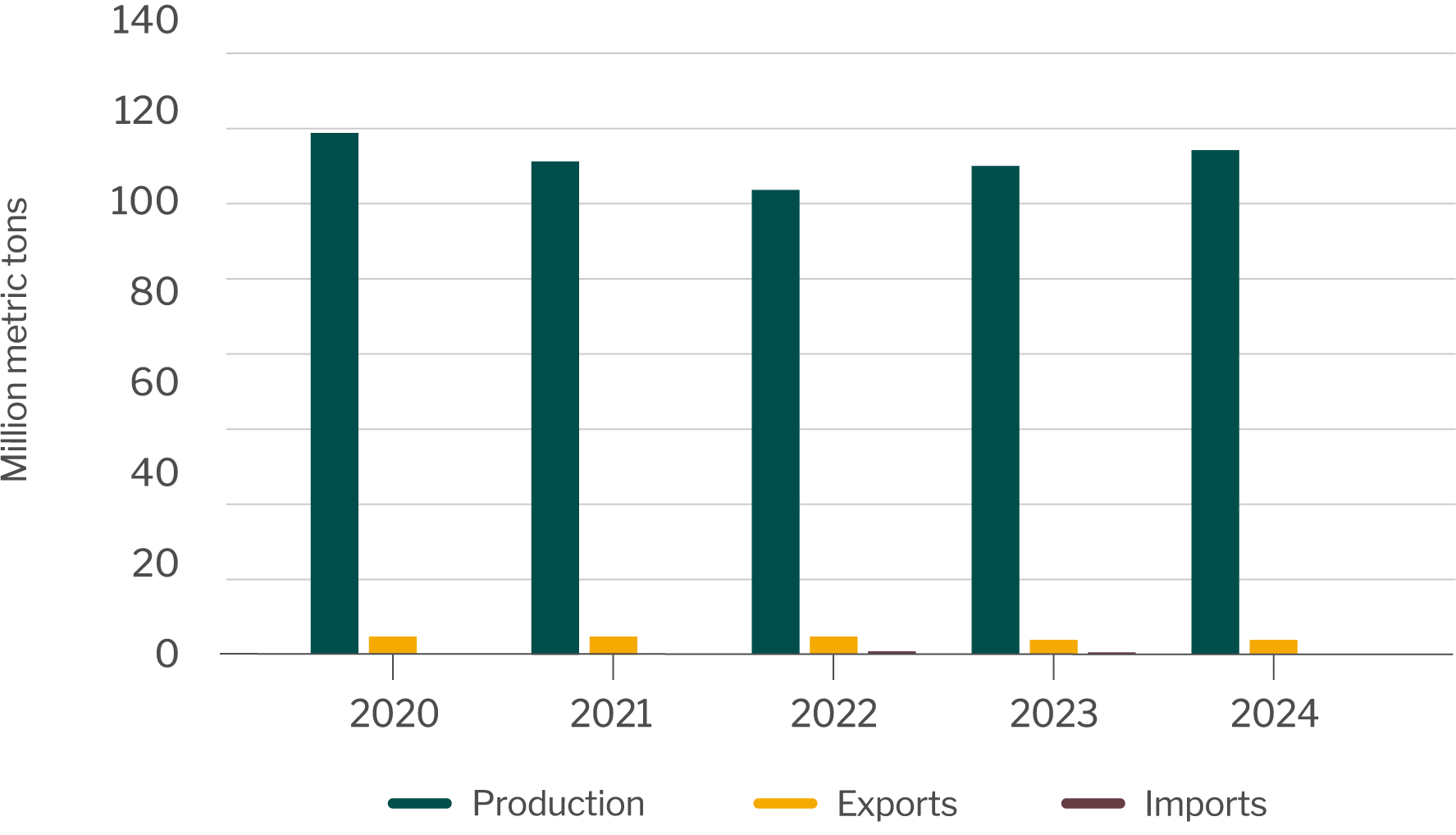

Exports make up 31% of the West Coast’s total hay production and about 3.1% of U.S. hay production. Higher quality hay is typically allocated for export markets, as these markets demand superior products and are willing to pay a premium for them. Key export destinations for West Coast hay producers include Japan, China, South Korea and Saudi Arabia. Long-standing markets like Japan and South Korea have remained stable over the years, providing consistent demand. Meanwhile, newer markets such as Saudi Arabia and the United Arab Emirates have shown significant growth, though they continue to be volatile.

China became the largest export market for West Coast hay in 2021, holding that spot through 2023. However, by 2024, China’s slowing economy and government initiatives to reduce dairy herds resulted in a sharp decline in hay imports, with reduced purchases expected to persist in the near term.

Hay imports for West Coast livestock producers are minimal, with most of them sourced from Canada.

Hay production, exports and imports

USDA National Agriculture Statistics Service. U.S. Census Bureau.

Tariff tracker - Tariff rates applied to U.S. trade partners are consistenly updated to reflect policy changes. The World Trade Organization (WTO) tracks duties and tariffs on hay and forages. For your convenience, the following links will take you to tariff data on alfalfa hay (a leading U.S. export for the hay industry) for top markets including Japan, South Korea and China. WTO also tracks rates for hay imports to the U.S. Please consult with a trade lawyer or professional for detailed and up-to-date insights on tariff rates and their application to hay.

For guidance on interpreting duty and tariff rates, please refer to our Tariff Guide.

Hay updates

Western producers see price improvements, but water remains the wild card.

Hay markets across the West are entering the second half of 2026 in a stronger position than a year ago, supported by higher prices, limited carryover stocks and steady demand. However, ongoing drought conditions, irrigation uncertainty and water allocation challenges remain the biggest risks to production and profitability through the remainder of the growing season.

Across AgWest's footprint, acreage trends remain relatively stable, suggesting supply-side adjustments are unlikely to significantly alter market dynamics through the remainder of the season.

Conditions by state:

Arizona

Hay quality has declined due to early-season heat, though demand for lower-quality forage remains supportive. Prices are generally around $200 per ton, with expectations for modest improvement if weather cooperates. Water availability remains a significant concern, particularly given anticipated Colorado River shortages and the potential for reduced allocations under future drought contingency plans.

California

Market conditions remain favorable, with producers reporting stronger prices than expected. In the Southern San Joaquin Valley, third cutting has been completed with no major yield or weather concerns due to irrigated production systems. Producers reported hay prices approximately $30 per ton above last year, with recent third-cutting alfalfa selling near $225 per ton. Demand appears supported by both dairy and retail channels. In Imperial Valley, growers are seeing prices around $200-$205 per ton, and continue utilizing deficit irrigation programs amid growing concerns about Colorado River water supplies and the potential for future allocation reductions.

Idaho

The market remains firm, with prices generally steady to $5 per ton higher than a month ago and above year-ago values. Demand is uneven, as some dairies remain on the sidelines while others actively contract supplies. Cattle ranchers have been among the most aggressive buyers due to ongoing drought concerns. Water availability remains the state's primary challenge. Several irrigation districts have warned of possible late-season water curtailments, prompting some growers to prioritize corn irrigation over hay production. Southern and eastern Idaho are increasingly concerned that reduced water allocations will limit second and third cuttings, while some farmers reliant on mountain runoff have already lost irrigation water. Well-irrigated operations are generally in a better position. Concerns are growing in eastern Idaho that many operations may only achieve a single cutting this year. Organic hay markets remain especially firm.

Montana

Dryland hay conditions in southern Montana range from poor to very poor due to spring freezes, drought, high temperatures, and wind. In contrast, northern Montana has recently received substantial rainfall, improving yield expectations to near-average or potentially above-average levels. Irrigated hay producers experienced poor first-cutting yields due to freeze damage but are optimistic about stronger second and third cuttings. Hay supplies remain tight, with much of the available crop already committed. New-crop high-quality alfalfa has sold between $225-$230 per ton, utility hay around $200 per ton, and wheat hay near $170 per ton. Strong cattle-sector demand and ongoing drought concerns continue to support prices.

Oregon

Hay growers are increasingly focused on water availability as drought conditions worsen. Several irrigation districts may impose water restrictions later this summer, creating concerns about maintaining production through subsequent cuttings. Despite these risks, first cutting has progressed well, with producers actively baling and preparing for second cutting. Demand for old-crop hay remains slow, while interest in new-crop supplies has improved. Hay quality and yields generally look favorable, aided by cooler temperatures and timely moisture. Baker Valley producers reported 2026 alfalfa sales near $250 per ton.

Washington

Market conditions continue to improve compared to 2025. Limited carryover inventories have supported higher prices, with alfalfa values generally running $20-$30 per ton above last year's levels. Higher-quality alfalfa is trading around $215-$220 per ton, feeder hay near $175 per ton, and premium Timothy horse hay between $235-$240 per ton. While profitability has improved, rain events during first cutting created some quality variability, though yields are generally average.

Profitability

June 10, 2026Hay (alfalfa): Slightly profitable - Bullish 12-month outlook

Hay (timothy): Slightly profitable - Neutral 12-month outlook

Tightening Western supplies and an expected reduction in hay production are helping rebalance the market, while increasing drought concerns are driving stronger domestic demand and improving alfalfa prices.

Sustained export demand, limited high-quality supply and steady forage demand are supporting timothy hay profitability despite higher production and logistics costs.

Exports make up 31% of the West Coast’s total hay production and about 3.1% of U.S. hay production. Higher quality hay is typically allocated for export markets, as these markets demand superior products and are willing to pay a premium for them. Key export destinations for West Coast hay producers include Japan, China, South Korea and Saudi Arabia. Long-standing markets like Japan and South Korea have remained stable over the years, providing consistent demand. Meanwhile, newer markets such as Saudi Arabia and the United Arab Emirates have shown significant growth, though they continue to be volatile.

China became the largest export market for West Coast hay in 2021, holding that spot through 2023. However, by 2024, China’s slowing economy and government initiatives to reduce dairy herds resulted in a sharp decline in hay imports, with reduced purchases expected to persist in the near term.

Hay imports for West Coast livestock producers are minimal, with most of them sourced from Canada.

Hay production, exports and imports

USDA National Agriculture Statistics Service. U.S. Census Bureau.

Tariff tracker - Tariff rates applied to U.S. trade partners are consistenly updated to reflect policy changes. The World Trade Organization (WTO) tracks duties and tariffs on hay and forages. For your convenience, the following links will take you to tariff data on alfalfa hay (a leading U.S. export for the hay industry) for top markets including Japan, South Korea and China. WTO also tracks rates for hay imports to the U.S. Please consult with a trade lawyer or professional for detailed and up-to-date insights on tariff rates and their application to hay.

For guidance on interpreting duty and tariff rates, please refer to our Tariff Guide.